Roadmap for banking reforms: Old wine in a new bottle?

A few days before the one-sided election of January 7, Prime Minister Sheikh Hasina asked voters to forgive her (and her party, I assume) for any mistakes that were made since the Awami League came to power, with a promise to rectify them if her party returned to office. And nothing, perhaps, requires as urgent a rectification as the AL's policy in regards to the country's banking sector.

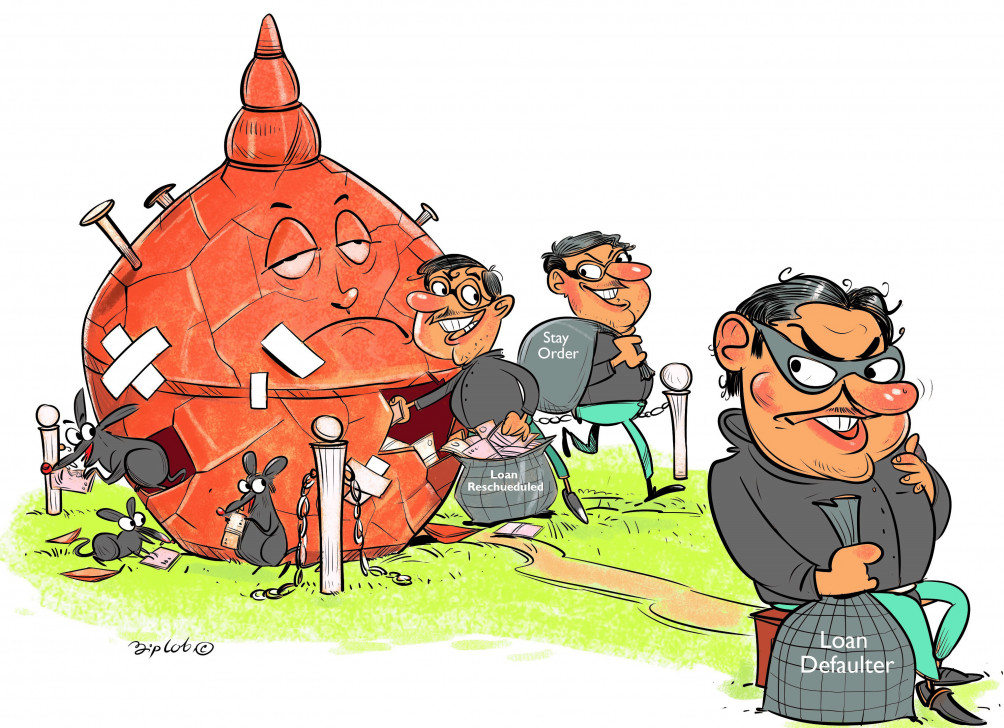

When the AL assumed office in 2009, the total defaulted loans amounted to Tk 22,481 crore, whereas at the end of September last year, non-performing loans (NPLs) stood at Tk 155,397 crore. During the last July-September period, NPLs in the banking sector decreased slightly. But that was only because Janata Bank rescheduled the defaulted loans of Beximco and S Alam, two of the country's biggest business groups which have received quite a few favours from the government. Such rescheduling tricks—which create the illusion of NPLs going down by hiding the figure from banks' balance sheets even though the liabilities still remain—have been at the core of the AL's banking sector policy. They have allowed the government—and vested interest groups—to continually hide the real amount of NPLs in the sector.

For all latest news, follow The Daily Star's Google News channel.

For all latest news, follow The Daily Star's Google News channel. According to Moinul Islam, a former professor of economics at Chittagong University, "If the entire amount of the loans involved in the court cases and the written-off loans are taken into consideration, the total bad loans in the banking sector will be Tk 450,000 crore." Similarly, according to economist Ahsan H Mansur, the actual amount of bad loans accounts for around 24-25 percent of the total loans disbursed, whereas via accounting tricks, this is being shown to be below 10 percent.

This buildup of NPLs, according to the Asian Development Bank (ADB), poses a serious risk to the health of banks' balance sheets and financial soundness, reducing interest income, lowering profitability, and depleting their capital bases. They also require higher risk weights and minimum loss coverage in banks' capital requirements, putting a strain on liquidity and increasing funding costs. Hence, it should come as no surprise that the central bank has had to provide increasing amounts of liquidity to credit-hungry banks.

According to Bangladesh Bank statistics, the central bank provided liquidity support amounting to Tk 633.47 billion to banks in June 2023. In the following month, the handouts more than doubled, to Tk 1.28 trillion. And since then, it has been rising every month, ultimately reaching Tk 3.63 trillion in January 2024.

According to a central bank official, if Bangladesh Bank does not "continue cash feeding to the banks as per their requirements," they "will be in severe liquidity crisis." Among other consequences, the interest rate would go up to a level that may be difficult for the economy to absorb. Already, a tight liquidity situation facing both the government and banks has pushed up yields of treasury bills and bonds, as well as the lending rate, in the banking sector. And overall, there is a lack of trust in the financial sector which is adversely impacting the country's economy.

With the banking sector in so much trouble and the authorities walking a tightrope to balance the economy and finance, the Bangladesh Bank on February 4 unveiled its roadmap for reining in defaulted loans and bringing good governance to the sector. The most obvious concern about it, of course, is how genuinely it will be implemented. Given our track record, proper implementation remains highly unlikely. Moreover, some of the action plans and policy reforms already exist or were added in the Bank Company (Amendment) Act, 2023. Yet, none of those prevented things from getting worse.

For example, the roadmap says that the banking regulator will provide necessary instructions to prevent lenders from exceeding the single-borrower limit. However, the same provision existed in the Bank Company Act for more than a decade. And yet, exceeding the single-borrower limit has become the norm in our banking industry, with around 89 borrowers of four state-run banks exceeding it as of June last year, as per a central bank report. What is worse is that, in its attempt to reduce the higher volume of bad loans in the banking sector, the roadmap further relaxed the loan write-off policy by letting banks write off from their balance sheet defaulted loans that have been in the "bad and loss category" for two years, down from three years previously. Again, this will only "artificially" reduce bad loans as the liabilities will remain—meaning that this so-called reform is just old wine in a new bottle.

In February 2019, the central bank lowered the timeframe to three years from five years. And what has that achieved? Default loans since then have gone up from Tk 943 billion to as high as Tk 1,560 billion.

During the discussions prior to the unveiling of the roadmap, the Bangladesh Bank governor was apparently told to bring down default loans by taking any measures necessary, including ignoring political pressure. After its unveiling, former BB Governor Salehuddin Ahmed said the central bank must have enough strength to tackle political interference and pressure from influential groups to implement the roadmap.

However, what is interesting is that back in January, central bank Governor Abdur Rouf Talukder said that the BB's activities have never been influenced by outside forces—a blatant farce of a statement that no one in their right mind would believe.

So, if the governor does not have the courage to even admit the fact that the central bank has bowed to political pressure time and again, has broken its own rules, and made special concessions for vested interests, how can he be counted on to have the courage to stand up to them now? And unless Bangladesh Bank can carry out the necessary reforms by standing up to political pressure—which will most definitely be there—this new roadmap will be nothing but another failed reformation plan.

It is time for the prime minister to prove that her promises to the people were legitimate, and ensure that the regulators have her backing in carrying out the reforms—in spite of any and all political pressure.

Eresh Omar Jamal is a journalist at The Daily Star. His X handle is @EreshOmarJamal.

Views expressed in this article are the author's own.

Follow The Daily Star Opinion on Facebook for the latest opinions, commentaries and analyses by experts and professionals. To contribute your article or letter to The Daily Star Opinion, see our guidelines for submission.

Comments