Only two options left for macroeconomic stability

Bangladesh does not have too many policy options other than reducing consumption of goods and services and making the exchange rate flexible in order to ensure macroeconomic stability, said a central bank report.

Although the government has tightened rules to contain imports since May after foreign currency reserves began sliding in the face of escalated import bills driven by the Russia-Ukraine war and supply disruptions, there has not been a significant decline in the purchase of goods and services from the international markets.

For all latest news, follow The Daily Star's Google News channel.

For all latest news, follow The Daily Star's Google News channel. On the other hand, the Bangladesh Bank has not allowed the exchange rate of the taka against the dollar to be determined by market forces despite repeated calls from local think tanks and economists long before the impacts of the war hit Bangladesh hard.

In September, the BB was compelled to adjust the exchange rate to a large degree in line with demand and supply to protect the reserves but the situation has not come under control completely.

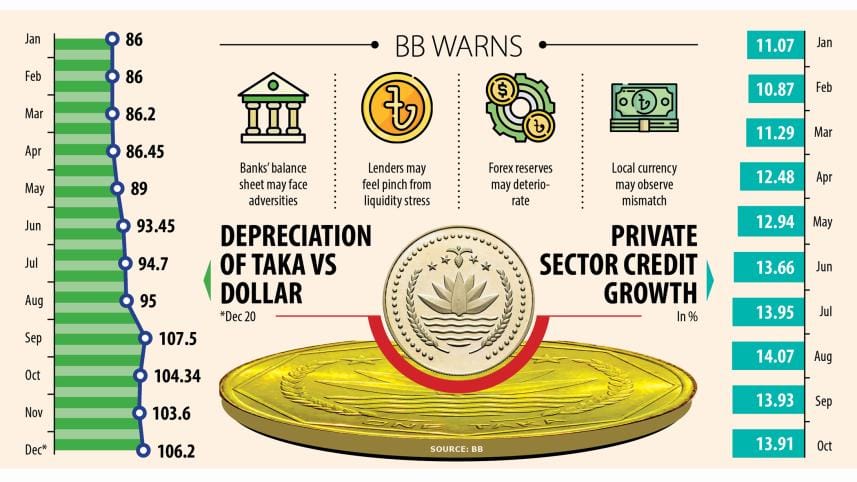

Owing to the dollar shortage, the taka has lost as much as 25 per cent of its value against the US dollar since the war began in February.

Now the central bank report says: "In view of tackling external factors-driven imported inflation, there are not many policy options available other than making appropriate supply-side interventions while managing the exchange rate adversities requires market-oriented flexibility."

It made the observation after carrying out a study styled "Impact of Exchange Rate and Global Commodity Price Inflation on Private Sector Credit in Bangladesh."

The BB yesterday published the research work carried out by its Chief Economist's Unit where it cited various risks emanating from the ongoing volatility in the country's foreign exchange sector.

The report said the unprecedented depreciation of the taka has contributed to the increase in the private sector credit growth at higher rates in recent times.

It, however, said the actual private sector credit growth is lower if the depreciation is considered. This is because the calculated weighted average growth rate of the exchange rate-adjusted private sector credit was much lower than the observed growth rates of credit.

Private sector credit growth stood at 13.91 per cent in October against the current fiscal year's target of 14.1 per cent set by the BB. The credit growth was 9.44 per cent in October last year.

Import payments stood at $25.5 billion in the first four months of this fiscal year, up 6.7 per cent a year ago.

Overall, adverse commodity price shocks and exchange rate volatility can create challenges to the economy through credit channels which ultimately impact the bank's balance sheet, the BB report warns.

A surge in import payments compared to export earnings leads to an increase in bank credit to the trade, which may create a potential liquidity mismatch.

The shocks could unfavourably impact economic activity and the ability of agents, including the government, to meet their debt obligations, thereby potentially deteriorating banks' balance sheets, the report said.

Large commodity price shocks can also affect bank balance sheets by weighing on the reserves and increasing the risk of currency mismatches.

A currency mismatch refers to how a change in the exchange rate will affect the present discounted value of future income and expenditure flows.

On top of that, a sharp increase in global commodity prices can impact commodity importers' budgetary balance, which may drive the government to adjust its budget to contain any such budgetary imbalance.

Speaking to The Daily Star, Md Habibur Rahman, chief economist of the central bank, says that both high import payments and private sector credit growth are largely influenced by global inflation.

The local currency has faced a remarkable depreciation in recent times, playing a significant role in pushing up both import payments and private sector credit growth.

"The central bank is now moving towards allowing the flexible exchange rates to tackle the situation," Rahman said.

"In addition, making appropriate supply-side interventions is also important to make the economy vibrant."

Under the supply-side intervention, import payments will be contained through the purchase of a lower volume of goods and services from the external sources, which may go on to cut consumption.

A central banker says that the government may face difficulties in providing subsidies in a consistent manner due to the imported inflation, which will subsequently create budgetary imbalance.

Comments