Why the reluctance to fund women's businesses?

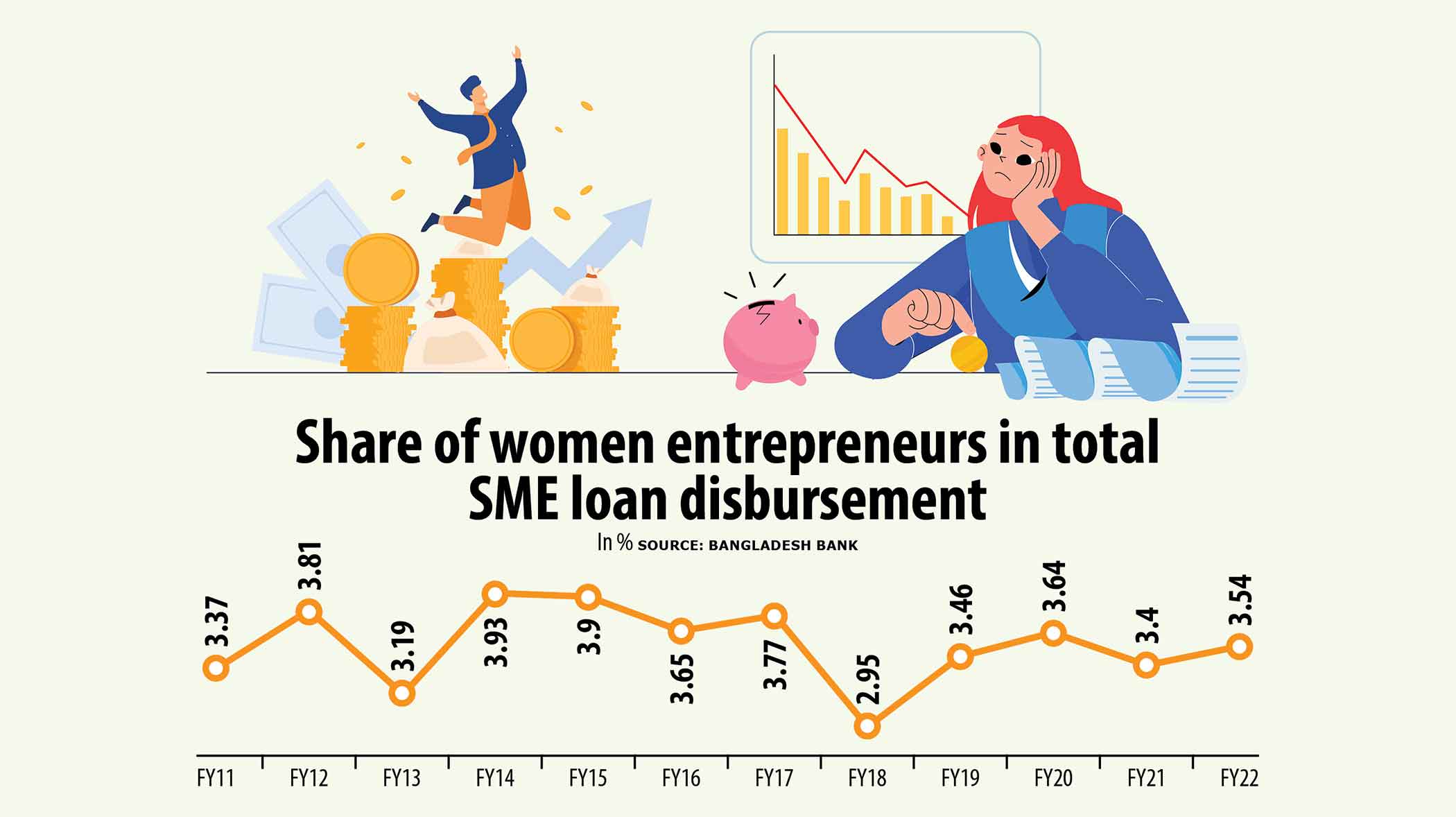

Although the number of women entrepreneurs has been growing in the country at an impressive rate, the share of total loans disbursed by banks and other financial institutions to women remains very low – at just 3.54 percent in the last fiscal year. It is disheartening that women entrepreneurs are lagging behind in terms of access to small and medium enterprise financing due to reluctance of the banks, despite the fact that the loan repayment rate of women entrepreneurs is almost 95 percent. Women report having to navigate myriad bureaucratic hurdles, stringent loan conditions, a cumbersome application process, and patriarchal attitudes of banks when accessing necessary finances.

For all latest news, follow The Daily Star's Google News channel.

For all latest news, follow The Daily Star's Google News channel.

We are disappointed that the positive initiatives of the Bangladesh Bank in recent times to facilitate the financial inclusion of women – including a circular issued in 2019 to banks to ensure 10 percent of the banks' total disbursements for cottage, micro, small and medium entrepreneurs (CMSME) to women – have not brought about the desired results. Many entrepreneurs complain that banks are only willing to lend to those who are already financially well-off. The application procedure itself is too convoluted and banks often ask for so many different documents that it is difficult, if not impossible, for many budding entrepreneurs to complete the process.

Providing collateral against loans has been identified as a major challenge, given the prevailing socio-economic situation of the country in which women already lack access to property and finances. It was highlighted in a recent seminar that as many as 75 percent of women have not applied for loans because of their inability to manage a loan guarantor. Yet others do not have the necessary knowledge or confidence to initiate the loan process.

Although the central bank has instructed all banks to give out Tk 25 lakh in SME loans to women entrepreneurs without any collateral, this has hardly been followed. Banks are also supposed to dedicate a desk to support women entrepreneurs in each of their branches and take proactive steps to fund women entrepreneurs who have not taken out loans from banks or financial institutions previously. The Bangladesh Bank must monitor and follow up with the banks to ensure that their instructions are being implemented.

We call upon financial institutions to ease women's access to loans, curtailing bureaucratic hurdles and simplifying the application process. Why must they insist on being so stringent when it comes to women, while lending out tens of thousands of crores, year after year, to known defaulters?

The government should also aim to increase financial literacy among women entrepreneurs through low-cost or cost-free literacy programmes. This support should not be confined to just two or three days of training, but should instead involve their business promotion and capacity building as well.

Comments