Is renewable deployment suffering from fossil fuel lock-in?

While the peak electricity supply reached 15,604MW in Bangladesh at the beginning of summer, many areas, mostly outside Dhaka, have been facing long hours of load-shedding and disruption of economic activities. The reason behind the current crisis is not the lower installed capacity, but the inability to buy imported energy to run the existing power plants and interrupted services due to technical inefficiency. It is tragic to see that while people are suffering from the crisis, over 40 percent of installed capacity remains idle. It is even more tragic that the new capacity addition of 660MW from the trial operation of Rampal and import of 748MW from Adani's Godda coal-based power plant could not be of any use to reduce people's suffering. On top of that, more committed power plants including Matarbari, Banshkhali, Rooppur nuclear power plant, and the second unit of Payra are waiting to be finished.

The question is no longer whether Bangladesh has the installed capacity to meet the electricity demand. Rather, the question is whether Bangladesh will be able to pay for the imported energy to fulfil its demand amid the US dollar crisis coupled with high international prices and dwindling foreign exchange reserves.

For all latest news, follow The Daily Star's Google News channel.

For all latest news, follow The Daily Star's Google News channel.

The excruciating summer temperature and the deteriorating power crisis in Bangladesh brought back the agenda of solar electricity. In this respect, recent policy developments need attention. The draft renewable energy policy set a target to increase the renewables' contribution to 40 percent by 2041. So far, the feasibility of the target has been discussed mainly from the technical and economic perspectives. Previous debates mostly focused on grid capacity, intermittent supply, battery use, demand management, etc. Another concern has been the high cost of solar power, until the cost declined globally over the last decade. Now, the new experiences of integrating renewables to the grid are widely known. Significant spillover of knowledge around the world made solar technology accessible to countries like Bangladesh. However, while the fossil fuel lock-in as a barrier to clean energy technology adoption is widely discussed in the West, it is yet to receive much attention in Bangladesh.

Technological lock-in refers to the situation of persistent failure to switch to a new technology as replacing the incumbent technology becomes highly expensive. Although the term has been used by economists, historians and sociologists since the 1980s, scholars have started to use "lock-in" in relation to fossil fuel use and the difficulty to switch to renewable energy. Others use the term carbon lock-in to describe a force that prolongs fossil fuel use despite knowing the risks of fossil fuels and having cost-effective alternatives. As a consequence, low-carbon technology diffuses at such a slow rate that the cost to society and the environment becomes too high.

Currently, many countries that are willing to phase out coal are finding it difficult to replace it, because it has already established a deep-rooted connection to society, institutions, and the economy. When a technology is adopted, it is not only about the energy it uses, it is also about the employment it creates, and the dependency it creates with the infrastructure, industry, and society. It is now very difficult for coal-dependent countries like Germany, India, Indonesia, and China to replace coal because it is expensive to replace the technology. The coal phaseout in those countries are slow, not only because the strong coal lobby resists phaseout, but also because it is expensive to compensate the workers, employ them elsewhere, and reorganise the infrastructure, economy, and institutions for clean energy use.

Considering the electricity overcapacity in Bangladesh created over the last decade, I want to say that Bangladesh, with its decisions to build coal power plants and an expensive nuclear power plant, has already started to feel the symptoms of technology lock-in. Even if Bangladesh wants to replace the existing technology with renewable technologies in the future, the possibility is getting weaker every day.

The investment of billions of dollars in LNG infrastructure, coal, and nuclear power plants over the last decade has already made the incumbent projects irreplaceable. It has already become difficult to implement a clean energy plan because of the existing overcapacity. Financing new renewable energy projects will most likely create some level or redundancy in the committed and existing installed capacity. Bangladesh's installed capacity of renewables is 966MW, which is 3.6 percent of the total installed capacity (26,700MW). The actual contribution to solar electricity supply is less than one percent (Ember 2023). By 2026, Bangladesh needs to install more than 1,500MW from renewable sources to reach the 10 percent target. The question is: don't we have to pay capacity charges to the idle plants? Obviously, we will have to pay unless the old ones are phased out.

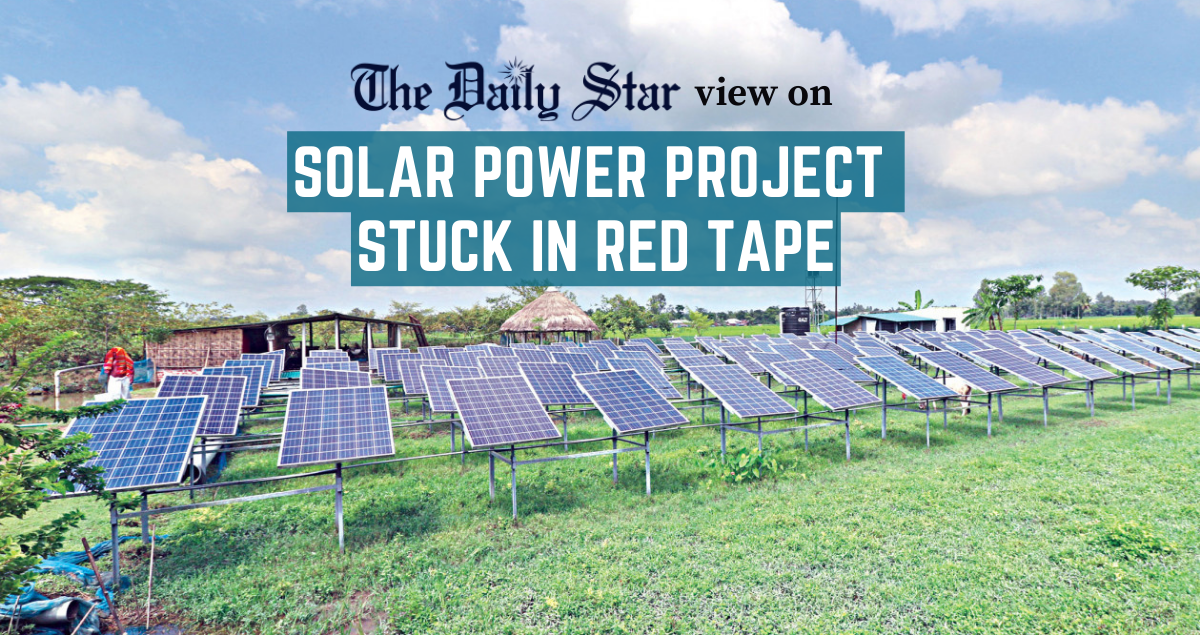

Currently, the existing on-grid installed capacity of solar power is 367.81MW. There are 550MW solar park projects committed; all are at the implementation stage. The 200MW solar power plant in Gaibandha is operating on trial. Although there are more at the planning stage, there is little understanding of whether they will be implemented or not.

Considering the electricity overcapacity in Bangladesh created over the last decade, I want to say that Bangladesh, with its decisions to build coal power plants and an expensive nuclear power plant, has already started to feel the symptoms of technology lock-in. Even if Bangladesh wants to replace the existing technology with renewable technologies in the future, the possibility is getting weaker every day.

The rising overcapacity is a concern not only because it is expensive now, but also because it will potentially reduce our ability to switch to cheaper alternatives. According to the new draft renewable energy policy, the targets to increase the renewable electricity supply are 2,500MW by 2026 (first phase), 8,000MW in 2026-2030 (second phase), and 24,000MW in 2030-2041 (third phase). The targets assume total installed capacity will be more than double (60,000MW) the current installed capacity (26,700MW) by 2041. It is also assumed that Bangladesh's GDP will grow above seven percent average. The Russia-Ukraine war, dollar crisis, rising inflation, forex reserve crisis, and poor economic performance do not seem to increase the demand as high as the predicted growth level. So, the new addition by committed power plants will more likely increase the burden as more plants need to remain idle.

The current gap between predicted and actual demand has questioned the reliability of the demand estimation. Even the past electricity demand estimation of the 2016 Master Plan was based on the assumption of 10 percent demand growth. The draft Integrated Energy and Power Master Plan (IEPMP) 2022 estimated that if the existing and committed power plants (gas, oil, coal, nuclear, and import) start production, by 2030 the total installed capacity will be 35,261MW. Based on various scenarios, the maximum demand in the same year will range from 31,709MW (low) to 41,890MW (high). After allowing for 10-15 percent reserve margin, the existing and already committed power plants will most likely satisfy the low scenario predicted demand, at the cost of limiting solar growth.

The existing coal-based capacity is 1,661MW, and committed capacity is 8,256MW. If more coal-based power plants are planned without considering the potential lock-in in the future, the electricity sector will again face a crisis. The persistent gap between actual generation and installed capacity has flagged the problem. It should ring the alarm now, rather than later when it will be even more difficult to replace the incumbent technologies. The government should learn from the crisis, revise the demand growth estimation based on more realistic assumptions, stop fossil fuel-based power plants, invest more on renewable deployment, and save the country from potential carbon lock-in. Expressing intention to transition to clean energy is not sufficient to save us from carbon lock-in.

Moshahida Sultana Ritu is associate professor of economics at the Department of Accounting and Information Systems, University of Dhaka.

Comments