Moody’s cuts banking outlook to negative

Moody's Ratings has downgraded Bangladesh's banking system outlook from "stable" to "negative", citing rising asset risks and worsening economic conditions.

The report, released yesterday, highlights key concerns, including deteriorating asset quality, high inflation, and weakening economic growth, which it says will negatively impact the banks' profitability and financial stability.

For all latest news, follow The Daily Star's Google News channel.

For all latest news, follow The Daily Star's Google News channel. "Structural risks to banks' asset quality, such as lax regulations and poor corporate governance, will persist," the US credit rating agency said.

Liquidity across the banking system is expected to be stable but tight, with the systemwide loan-to-deposit ratio standing at 81 percent as of September 2024, according to the report.

Moody's acknowledges that the government is likely to continue supporting banks through regulatory forbearance and liquidity measures to reduce "contagion risks".

Such measures would mask asset risks and hamper loan recovery, Moody's said. The systemwide NPL provision ratio remained low at 42 percent as of the end of June 2024, which would decrease even further if loans with modified payment terms are included.

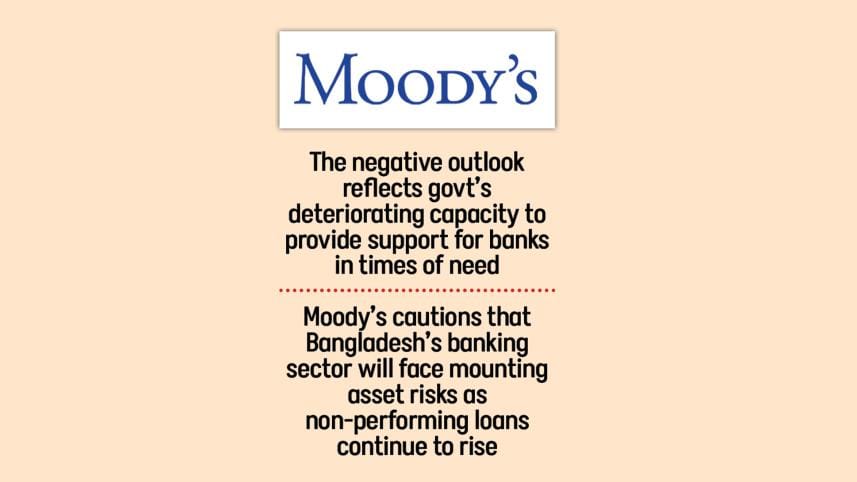

The negative outlook also reflects the government's deteriorating capacity to provide support for banks in times of need, the report said.

The report further cautions that Bangladesh's banking sector will face mounting asset risks as non-performing loans continue to rise.

As of September 2024, the systemwide NPL ratio had surged to 17 percent from 9 percent in just nine months.

"Asset quality will deteriorate as the operating environment worsens," Moody's said, adding that "social unrest has severely affected" the financial stability of some domestic businesses by reducing demand, disrupting supply chains, and creating labour shortages.

Additionally, newly introduced stricter NPL classification rules taking effect in April 2025 could further exacerbate the situation, the agency said.

According to Moody's, the banks' profitability will deteriorate as loan-loss provisions increase. Loan-loss provisions will increase significantly across the system as existing reserves for stressed loans are insufficient, especially in light of rising asset risks.

Banks with strong fundamentals will see improvements in net interest margins (NIMs) as lending rates remain elevated after the removal of an interest rate cap by the central bank while benefitting from decreases in deposit costs amid a flight to safety among depositors.

On the other hand, NIMs for banks with worsening asset quality will decline as the proportion of interest yielding loans shrinks.

The agency projects Bangladesh's real GDP growth will slow to 4.5 percent in the fiscal year ending June 2025, from 5.8 percent the previous year.

"The operating environment will deteriorate due to economic slowdown and a high inflation rate," Moody's said.

The slowdown is driven by a combination of political and social instability, disruptions in supply chains within the garment sector, and weakening demand, both domestically and internationally.

Furthermore, Bangladesh's central bank has raised policy rates from 6 percent to 10 percent over 15 months in an attempt to curb inflation, which is expected to remain high at 9.8 percent in 2025.

High inflation and unemployment rates will limit the interim government's political capital to implement significant reforms, according to the report.

The interim government's fiscal capacity to provide support will be limited and deteriorating, further constrained by its lack of political power, the report observes.

Despite these challenges, Moody's noted overall capitalisation is expected to remain stable due to slower credit growth.

However, state-owned banks remain particularly vulnerable, with an average capital-to-risk-weighted-assets ratio of -2.5 percent as of September 2024, well below the private sector average of 9.4 percent and regulatory minimums.

"State-owned banks will remain undercapitalised because of weak profitability that is strained by high levels of NPLs and the absence of government capital infusions," Moody's said.

Comments