Evolution of Digitalization in Bangladesh’s Financial Sector

Bangladesh's financial sector has undergone a paradigm shift, experiencing a surge in digitization over the last one-and-a-half decades, bringing millions under banking services that have even reached the village level.

In addition to modernizing the traditional banking system, the introduction of Mobile Financial Service (MFS), payment services, and fintech has played a vital role in adopting technology in the country's financial sector.

For all latest news, follow The Daily Star's Google News channel.

For all latest news, follow The Daily Star's Google News channel. Internet Banking

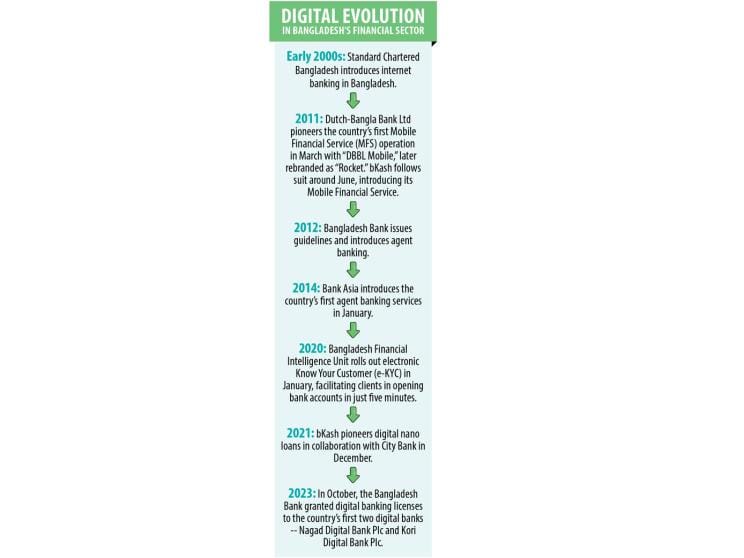

The country's online banking first started in the early 2000s with Standard Chartered Bangladesh, and ever since, it has rapidly integrated into the banking industry.

In 2010, banks began taking up a wide range of initiatives as part of their efforts to encourage customers to adopt the digital window.

Thanks to the growing use of internet banking, people can now deposit and transfer funds anytime, from anywhere, eliminating the necessity to visit a physical branch of a bank.

The number of Internet Banking Customers was 76.32 lakh as of August '23, and its transactions were Tk 52,099.67 crore in the same month, an increase of 104 percent year-on-year from Tk 25,543 crore, according to data from Bangladesh Bank.

Agent Banking

In 2012, Bangladesh Bank introduced agent banking in the country by issuing guidelines, aiming to provide a safe alternate delivery channel of banking services to the underprivileged and underserved population who generally live in geographically remote areas beyond the reach of traditional banking networks.

Bank Asia introduced the country's first agent banking services in January 2014. Besides the sharp growth in transactions, the number of accounts opened by agents has also increased year-on-year. The number of agents across the country stood at 15,671 as of August 2023, while it was 14,509 in the same month the previous year. The number of agent banking outlets rose to 21,559 from 19,981 during the period. The total number of agent banking accounts stood at 2.04 crore in August 2023, up by about 23 percent from the same month a year earlier.

CRM

Banks in Bangladesh are consistently introducing new technology to make banking services easier for customers. Cash recycling machines (CRMs) are one such technology that transforms the country's financial sector. The new technology allows users to deposit and transfer cash to others' accounts. In Bangladesh, banks started setting up CRMs in 2017. As of August this year, the number of machines was 3,652, up from 1,930 a year ago, according to data from Bangladesh Bank.

e-KYC

Opening an account has always been a cumbersome task for customers. In January 2020, the Bangladesh Financial Intelligence Unit (BFIU) rolled out the Electronic Know Your Customer (e-KYC), facilitating clients to open bank accounts in just five minutes, a procedure that previously took two to four days.

Mobile Financial Service (MFS)

Over a decade ago, access to financial services were unavailable and unaffordable for many individuals and businesses in Bangladesh. In 2011, the Mobile Financial Service (MFS) was introduced in Bangladesh, with 27 banks obtaining approval from the central bank. Not all licensees saw the light of the day. However, 19 firms rolled out the service by 2016. Of these, 13 entities currently operate in a market that witnesses more than Tk 3,500 crore worth of transactions every day, and the amount is increasing day by day. Dutch-Bangla Bank Ltd pioneered the country's first MFS operation in March 2011 with its "DBBL Mobile," later rebranded as "Rocket." Besides, bKash, a subsidiary of BRAC Bank, followed suit three months later. The number of MFS accounts stood at 21.24 crore in August 2023, and the number of transactions was Tk 51.22 crore in the same month.

Digital Nano Loans

The recent move, the "digital nano loan," is displaying promising prospects thanks to the instant and on-time disbursement of loans ranging from Tk 500 to Tk 50,000 to individual customers at up to 9 percent interest. About 1.6 lakh customers have already availed the loans from lenders, and the default rate is less than 1 percent, according to the banks.

In December 2021, bKash pioneered the digital nano loan in collaboration with City Bank, introducing the Digital Nano Loan targeting small borrowers, including cottage, micro, small, and medium enterprises (CMSMEs), and even for personal use. Since its launch, at least three more banks have introduced similar products, and all of them express optimism about the future of digital lending.

After a successful pilot, Prime Bank commercially launched its digital nano loan product, PrimeAgrim, in October 2022. Dhaka Bank has launched e-Rin products, while Bank Asia launched the digital nano loan on a pilot basis.

"Bangladesh has been experiencing rapid financial inclusion in sync with faster adoption of digital technology," said Atiur Rahman, former governor of the central bank. "The digitization of the financial sector gained new momentum through the latest move by Bangladesh Bank toward digital banking," he said.

Digitization of financial services has revolutionized access to finance in Bangladesh. This will be pivotal in making the country's economic recovery desirably inclusive.

At the same time, special care needs to be taken to ensure that digital infrastructure and access to the internet become affordable and sustainable, he added.

Anis A Khan, a former chairman of the Association of Bankers Bangladesh, said Bangladesh has a high demand for financial technology products. The financial institutions have taken a great stride in the development of the digital platform and customer-friendly sophisticated products for customers, he added.

Now, with the emergence of nanotechnologies and artificial intelligence, financial institutions must ready themselves for a revolutionary shift in financial technologies," he emphasized.

According to Prof. Shah Ahsan Habib from the Bangladesh Institute of Bank Management (BIBM), a supportive policy and regulatory environment are the crucial prerequisites for the digitization journey of the financial sector.

Comments