A reality check for the renminbi

After years of speculation and false starts, it seems that the internationalisation of the renminbi is well underway. On March 29, China and Brazil announced plans to trade using their own currencies, rather than the US dollar. The day before, the China National Offshore Oil Corporation and France's TotalEnergies completed their first-ever renminbi-denominated liquefied natural gas (LNG) trade. Russian President Vladimir Putin recently said he wanted to use the Chinese currency not just for trading with China, but also as a form of payment in trade with other countries in Asia, Africa, and Latin America. And Saudi Arabia has been in talks with China since last year about accepting payments for some oil exports in renminbi.

It is no secret that China would like to convert the renminbi into an international currency and move away from the global dominance of the US dollar. While this is often interpreted as a geopolitical move, a way to insulate China from possible US-led economic sanctions in the future, transforming the renminbi into one of the world's leading settlement currencies would also greatly benefit the Chinese economy. Moreover, it would help protect the country from an exchange rate crisis, which is why other countries, including India and ASEAN member-states, are trying to internationalise their currencies, too.

For all latest news, follow The Daily Star's Google News channel.

For all latest news, follow The Daily Star's Google News channel.

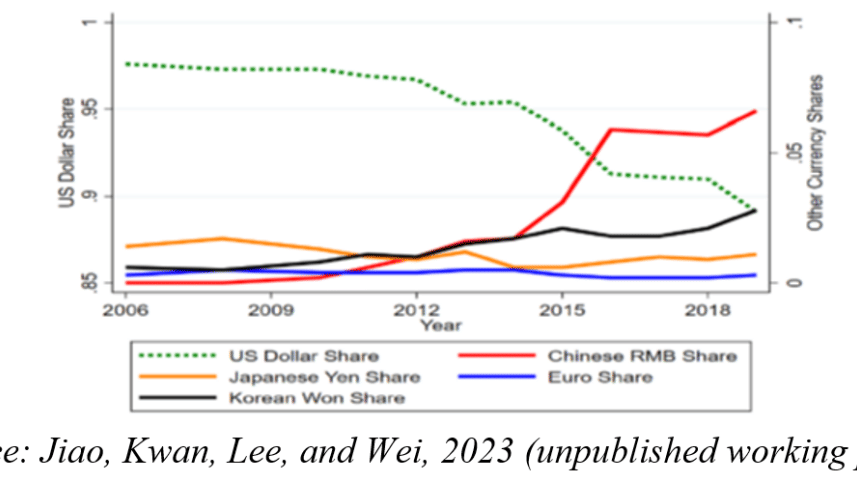

The figure below, based on ongoing research by my co-authors and me, illustrates the progress that China has made in its efforts to internationalise the renminbi. The red line traces South Korean firms' renminbi-denominated exports as a share of its total exports to China between 2006 and 2020, showing the Chinese currency's share rising from zero percent before 2008 to nearly six percent by 2020. In October 2016, the renminbi became part of the basket of currencies underpinning the International Monetary Fund's (IMF) reserve asset, special drawing rights, joining an exclusive club alongside the dollar, the euro, the yen, and the British pound.

While these are impressive milestones, one should not exaggerate the degree to which the renminbi is encroaching on the greenback's position. As the figure shows, the US dollar's share of South Korean exports to China declined from nearly 98 percent in 2006 to roughly 87 percent in 2020. In other words, the dollar has gone from overwhelmingly dominant to slightly less dominant. Even in China-South Korea bilateral trade, the renminbi is not even close to displacing the dollar.

Moreover, roughly 99 percent of South Korean exports to the US during the same period were denominated in dollars; none were denominated in renminbi. By contrast, the dollar's share of South Korean exports to Japan was 45 percent, about equal to that of the yen, with the won and the euro accounting for the rest. In other words, the US dollar continues to dominate global trade, including bilateral trade not involving the US, while the renminbi is essentially used only in transactions involving China.

It is no secret that China would like to convert the renminbi into an international currency and move away from the global dominance of the US dollar. While this is often interpreted as a geopolitical move, a way to insulate China from possible US-led economic sanctions in the future, transforming the renminbi into one of the world's leading settlement currencies would also greatly benefit the Chinese economy. Moreover, it would help protect the country from an exchange rate crisis, which is why other countries, including India and ASEAN member-states, are trying to internationalise their currencies, too.

Part of the reason for the greenback's continued pre-eminence is that, in addition to its status as a trading power, the US has very large and liquid capital markets where foreign investors can park their dollar-denominated assets. Because of its capital controls, China's domestic financial market is far less liquid, making the renminbi unattractive to international investors.

Theoretically, China could raise the renminbi's global profile by loosening capital controls. But doing so could come at a significant cost, exposing the Chinese economy to the (often negative) consequences of US interest-rate movements and global financial cycles. Moreover, premature capital-account liberalisation could exacerbate the existing distortions within China's financial system, where domestic savings are not always channelled to the most productive firms. The Chinese authorities are keenly aware of these risks, which is why they have been prioritising financial stability over renminbi internationalisation.

There are, however, other ways to promote the renminbi. A series of currency swap agreements between the People's Bank of China (PBOC) and its counterparts in other countries, for example, could help make the renminbi less risky for international firms and investors.

In addition, a digital renminbi could facilitate partial capital account liberalisation without formally removing capital controls. By removing the anonymity of foreign investors, a digital renminbi would allow the PBOC to limit cross-border financial transactions to less volatile types and more conveniently activate a circuit-breaker when needed. Being able to separate inflows of "hot money" from more stable types of foreign investment could convince the central bank to relax some capital controls and allow financial capital to flow more freely.

In sum, while China has achieved notable progress towards making the renminbi a global reserve currency, it is still far from reaching its goal. While it could use a digital currency to deliver de facto partial capital account liberalisation, it will not undermine the dollar's hegemony without going much further in loosening capital controls.

Shang-Jin Wei, a former chief economist at the Asian Development Bank, is professor of finance and economics at Columbia Business School and Columbia University's School of International and Public Affairs.

Copyright: Project Syndicate, 2023

www.project-syndicate.org

(Exclusive to The Daily Star)

Comments