Tax exemptions stood at Tk 1.07 lakh crore in FY23

Bangladesh’s direct tax expenditure -- comprising rebates, exemptions, and concessional tax rates -- fell 8 percent year-on-year to Tk 1.07 lakh crore in fiscal year 2022-23, according to data published by the National Board of Revenue (NBR) yesterday.

Tax expenditure, often described as implicit subsidies extended through the tax system, stood at 2.39 percent of GDP in FY23, down from 2.9 percent a year earlier.

For all latest news, follow The Daily Star's Google News channel.

For all latest news, follow The Daily Star's Google News channel. Corporate income tax accounted for the bulk of the expenditure at Tk 73,989 crore, representing 69 percent of the total.

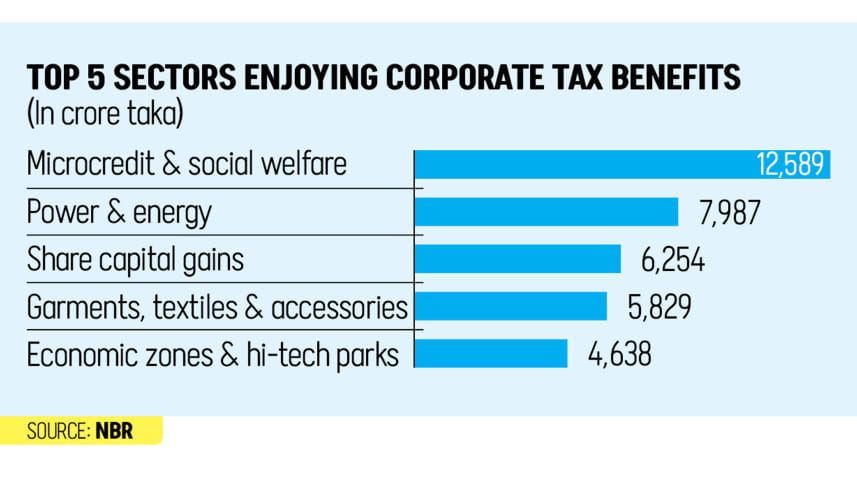

These benefits were largely concentrated in sectors such as microcredit and social welfare, power and energy, and garments, textiles, and accessories.

Among corporate tax expenditures, the highest allocation went to the microcredit and social welfare sector, amounting to Tk 12,589 crore, or 17.01 percent of the total corporate tax expenditure.

The power and energy sector followed with Tk 7,987 crore, equivalent to 10.79 percent.

Tax expenditure related to share capital gains stood at Tk 6,254 crore, accounting for 8.45 percent.

The garments, textiles, and accessories sector received Tk 5,829 crore in tax expenditure, making up 7.88 percent of the total.

Meanwhile, incentives for economic zones and hi-tech industries, aimed at promoting industrial diversification and infrastructure development, amounted to Tk 4,638 crore, or 6.27 percent.

On the other hand, personal income tax expenditure was estimated at Tk 33,143 crore, comprising 31 percent of the total, with a significant portion attributed to salary-related relief measures.

“The fiscal cost of tax expenditures in Bangladesh remains substantial,” the report said.

The NBR called for tax expenditures to be more strategically designed and periodically evaluated against key policy priorities, including export diversification, green energy transition, SME development, women’s economic empowerment, and regional equity.

The report suggested that existing incentives, such as tax holidays, could be better aligned with emerging national priorities.

For instance, these could be repurposed to support climate-resilient infrastructure or promote digital entrepreneurship in underserved regions.

Emphasising the need for a more transparent and accountable system, the report said a well-calibrated approach -- balancing revenue imperatives with growth incentives, equity, and social inclusion -- would allow Bangladesh to transform its tax incentive regime into a more effective instrument of economic policy, aligned with its long-term development aspirations.

Comments