From ‘basket case’ to billion-dollar borrower

When Bangladesh emerged from a bloody war of independence in 1971, the economy was devastated, institutions were fragile, and resources were scarce. Foreign grants became a lifeline for rebuilding the country.

The situation was so severe that economists Just Faaland and JR Parkinson described Bangladesh in 1976 as a “test case for development”. In their book, they argued that while trade mattered, foreign aid was the most important factor behind the country’s long-term growth. Many observers predicted permanent aid dependence, while some international commentators labelled Bangladesh a “basket case”.

For all latest news, follow The Daily Star's Google News channel.

For all latest news, follow The Daily Star's Google News channel. More than five decades later, those forecasts have not materialised. In 2012, The Economist published an article titled “Out of the basket” on Bangladesh’s progress, while also noting the “Bangladesh puzzle” of strong social gains despite economic shortcomings.

How Bangladesh reached this point, and where it goes next, is more complex than a simple success story.

THE LONG GOODBYE TO GRANTS

In the decades following independence, donor countries and international organisations channelled large amounts of funding into Bangladesh with little or no repayment obligation. These resources helped rebuild infrastructure, strengthen food security, and expand health and education services.

“Foreign grants at that point were equivalent to seven or eight percent of GDP,” said Debapriya Bhattacharya, distinguished fellow at the Centre for Policy Dialogue (CPD).

Over time, agricultural production improved, industries expanded, and the garment sector emerged as a global export powerhouse. Remittances from migrant workers added a steady source of foreign exchange.

“Remittances and RMG exports together have helped Bangladesh move away from reliance on foreign aid. That, in itself, is a very healthy sign,” said Selim Jahan, a former director at the United Nations Development Programme (UNDP) Human Development Report Office.

As the economy grew, foreign aid declined in relative importance. Today, aid accounts for less than one to two percent of GDP.

“Although dependence on aid has declined, this is largely due to overall economic growth, not a deliberate financing strategy,” Debapriya said.

LOANS STEP IN, GRADUALLY

Grants did not disappear because Bangladesh became independent of external finance. Instead, concessional loans gradually replaced them.

Multilateral institutions, including the World Bank, the Asian Development Bank, and the Asian Infrastructure Investment Bank, became major financiers of development projects. Bilateral partners such as Japan and China also increased lending, particularly for large infrastructure investments.

At independence, Bangladesh received $461 million in foreign assistance, including $218 million in grants. By fiscal year 2024-25, the country received $5.16 billion in external assistance, of which only 7 percent came as grants, with the remainder as loans.

By fiscal year 2024-25, Bangladesh had secured nearly $200 billion in total external commitments, with almost $140 billion disbursed, according to Economic Relations Division (ERD) data. Of the disbursed amount, $30 billion came as grants and the remaining $110 billion as loans.

Zahid Hussain, former lead economist at the World Bank’s Dhaka office, said the transition reflected structural change.

“There was a time when, without grants, the economy could not function. Grants were seen as the only financing option,” said Hussain. “The economy has moved away from that position through structural transformation. Development cannot happen through grants alone.”

He added that many so-called grants were actually concessional credits from the World Bank Group’s International Development Association.

“Even what we call ‘grants’ are often not technically grants. World Bank Group’s International Development Association provides concessional ‘credits’ with very soft terms, which made borrowing affordable for decades.”

Those loans helped keep financing costs low.

“Compared to commercial loans, borrowing costs are still significantly lower. This remains an opportunity, not a dependency,” Hussain said.

THE DEBT CLOCK TICKS

That opportunity may become harder to sustain.

Bangladesh is preparing to graduate from the United Nations’ least developed country (LDC) category, a transition that will eventually reduce access to preferential financing and trade benefits.

“Even if LDC graduation is delayed, in a few years, we will reach a point where grants will no longer be available. We will have to depend on market-based loans, and those must be repaid. That will be both a burden and a challenge,” said Jahan.

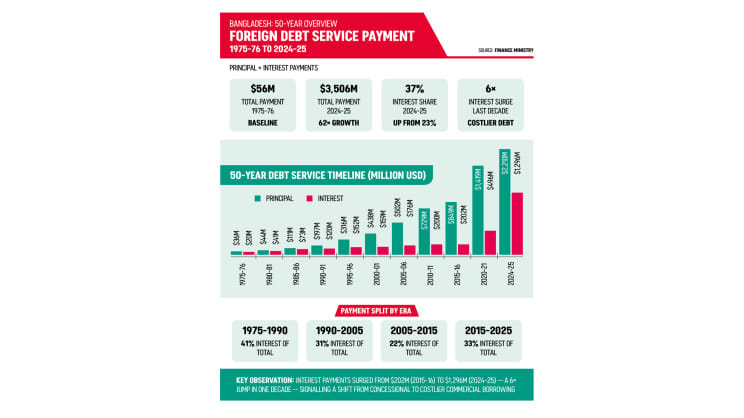

Debt-servicing costs have risen sharply. Bangladesh paid $56 million in principal and interest on external debt in 1975-76. By 2024-25, the figure had increased to $3.5 billion.

Through April of the current fiscal year, external debt servicing had already reached $3.8 billion. Including domestic liabilities, repayment obligations are much larger.

Repayment of principal and interest on overall public debt is expected to exceed $30 billion this fiscal year, increasing pressure on public finances.

IS THERE CAUSE FOR CONCERN?

The trajectory of external interest payments reinforces this concern.

Jahan pointed to wider global risks.

He said, “The geopolitical environment is not favourable. Our dependence on imported oil and gas means our import costs will rise, and these must be paid in foreign currency. At the same time, the global situation raises uncertainty about how much we can expand exports.”

He also flagged a caution from the IMF. “The volume of loans has increased substantially, and interest payments are rising. There is a real risk, something even the IMF has cautioned, that we may be moving towards an unsustainable situation.”

In its Asian Development Outlook (ADO) released in April, the Asian Development Bank (ADB) projected public debt at 42.4 percent of GDP by the end of the current fiscal year, up from an estimated 42.1 percent in FY2025.

The ADB noted that Bangladesh has so far avoided a public debt default but warned that signs of vulnerability require strategic action to protect fiscal sustainability.

In January this year, the International Monetary Fund said total public and publicly guaranteed (PPG) debt stood at $188.79 billion, or 41 percent of GDP, in fiscal year 2024-25, up from 39 percent a year earlier. The total included $101.24 billion in domestic debt and $87.55 billion in external debt.

The ADB also stressed the importance of maintaining foreign-exchange reserves. Reserve buffers have fallen from more than 75 percent of total external debt in 2016 to just 21.5 percent in 2023.

Although external debt has remained broadly stable at around 22 percent of gross national income, weaker reserves have reduced Bangladesh’s capacity to absorb shocks and increased vulnerability to liquidity pressures.

“The rapid growth of public debt and debt service costs, together with low foreign exchange reserve buffers, point to the need for improving debt management.”

READING THE NUMBERS CAREFULLY

Not all economists view the situation with alarm.

Rizwanul Islam, former special adviser at the International Labour Organization (ILO), argued that debt should be assessed in a broader economic context.

“Debt, whether external or domestic, should not be viewed in isolation. It must be analysed alongside GDP, exports, reserves, and overall economic performance,” he said.

At around 23 percent of GDP, external debt does not signal immediate danger by conventional measures, and short-term debt remains manageable.

But he warned against complacency.

“The real concern lies in the nature of growth. Narrow export dependence, limited diversification, and weak resilience to external shocks,” said Islam.

He also noted a structural mismatch: “Disbursement of loans and repayment obligations have not always been well synchronised, which creates additional stress.”

Debapriya challenged the view that debt-to-GDP ratios alone determine safety.

“The real concern is not the size of debt, but the country’s ability to repay it in foreign currency,” he said. “The idea that borrowing up to 30-40 percent of GDP is harmless is misleading.”

He pointed to weak project planning and rising borrowing costs, adding, “At present, it is uncertain whether Bangladesh is heading toward a debt crisis, but the risks are increasing.”

Towfiqul Islam Khan, additional director of research at CPD, argued that fiscal space and foreign-exchange reserves are more important than headline debt ratios.

He said, “Bangladesh’s debt burden is rising, but the debt-to-GDP ratio alone does not tell the full story. The real question is whether the country has enough fiscal space and foreign exchange reserves to meet its repayment obligations.”

Khan said returns from debt-financed public investments have often lagged expectations, while revenue growth has failed to keep pace with economic growth. Cost overruns, project delays and weak project appraisal have further reduced the effectiveness of borrowing.

“Cost overruns, project delays and weak project appraisal have increased the risk that public borrowing will not generate adequate economic returns,” he said.

He also argued that official debt projections have often relied on overly optimistic assumptions while emerging vulnerabilities were underestimated.

“Debt projections have frequently been based on overly optimistic assumptions, while emerging vulnerabilities were underestimated by policymakers and insufficiently flagged by international institutions.”

THE FDI GAP

One issue repeatedly emerges in discussions about external finance: foreign direct investment (FDI).

“Bangladesh has not been able to attract sufficient foreign direct investment,” said Debapriya. He noted that much of the inflow remains concentrated in export processing zones with limited links to the wider economy.

Unlike loans, FDI creates no repayment obligation. A broader and more diversified investment base could reduce pressure on borrowing as a source of development finance.

Economists broadly agree that the challenge is not necessarily borrowing less, but borrowing more effectively.

Islam argued that debt should be evaluated against GDP, exports and reserves, while ensuring that borrowed funds support productive investment rather than routine budget financing.

“There is no alternative to broadening the economic base, diversifying exports, and strengthening sources of foreign exchange,” he said.

Debapriya called for a comprehensive debt management strategy built on transparent reporting, regular policy reviews and careful assessment of borrowing capacity.

Jahan stressed the importance of choosing financing sources wisely.

“We may have to take on more loans, but the critical question is, from where? Multilateral financing is declining, and bilateral sources come with various conditions. We need to carefully determine our approach.”

Hussain summarised the challenge succinctly.

“Debt is an opportunity, but if poorly managed, it can turn into a crisis.”

Comments