Deposit, Credit Disbursement

PCBs outstrip NCBs for the first time

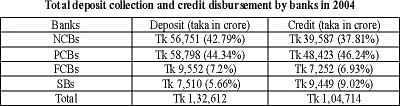

Rejaul Karim Byron

Despite shiring only 23 percent of total bzanch network, private commercial banks (PCBs) for the first time in Bangladesh banking history have overtaken nationalised commercial banks (NCBs) in terms of deposit and credit disbursement in 2004. With the recent developments in banking sector in 2004, private banks broke the historical dominance of public banks in credit disbursement. The 29 PCBs having a network of 1,488 branches registered 44.34 percent share in deposits while four NCBs with their 3,390 branches throughout the country recorded 42.79 percent in the last calendar year. Analysts attribute the success of PCBs to fierce competition among private banks. The competition to woo clients and emulate one another is so intense that one bank lures efficient staff of another bank offering higher facilities to get better edge. PCBs often introduce new and diversified financial products to provide wider option to customers. PCBs also offer greater salary, incentives and training to their staff. On the o|her hand, staff of NCBs lack spirit as they get few facilities from their organisations. PCBs often buy veteran and expert hands from NCBs offering better financial facilities. The PCBs also grabbed 46.24 percent of the total advance while the NCBs contributed 37.81 percent. Foreign commercial banks and specialised banks handled rest of the share in deposit and advance. In 2004, PCBs registered 25.6 percent growth in deposit and 26.8 percent in advance while NCBs saw only 8.1 percent growth in deposit and 8.05 percent in advance. Meanwhile, overall deposit growth was 16.3 percent and advance 16.49 percent. The banking sector deposit stood at Tk 1,32,612 crore and credit at Tk 1,04,714 crore. Second and third generation private banks were credited for the tremendous success of PCBs which achieved 31 percent to 136 percent deposit growth and 28 percent to 107 percent growth in advance. A deputy general manager of a public bank recently took a job in Mutual Trust Bank where he will get financial benefit worth about Tk 1 lakh per month while he got Tk 30,000 worth benefits from his previous employer. "I appeared in promotion exams of my bank for a number of times but it did not work. Without nepotism and lobbying, there is little scope for promotion in NCBs. With loer financial benefits and bleak prospect of promotion, why should I languish in a state-run bank," an aggrieved officer of an NCB told The Daily Star. Many officers of NCBs also voiced the similar frustration. A high ranking official of National Credit and Commerce Bank said, "At private banks we offer lucrative facilities to staff and at the same time extract maximum work from them. We want efficiency." An NCB official impute poor performance of NCBs to a central bank embargo on credit ceiling. As NCBs are struggling to reduce bad debt, |he central bank put credit grow|h restriction to five percent. Lue to the cap, NCBs could not put efforts on deposit mobilisation. Deposit in PCBs stood at Tk 58,798 crore and credit at Tk 48,423 crore. Deposit in four NCBs amounted to Tk 56,751 crore and credit Tk 39,587 crore. The 10 foreign commercial banks(FCBs) achieved a deposit of Tk 9,552 crore and credit Tk 7,252 crore in 2004 posting a growth of 13 percent in both segments. Deposits in nive specialised banks (SBs) amounted to Tk 7,510 crore and advance Tk 9,449 crore in the same period registering a growth of 19.89 percent and 9.16 percent.

|